Last Updated: May 16, 2026

Kern County homeowners are sitting on one of the most overlooked financial opportunities in California right now. Zero-down solar options Kern County residents can access have expanded significantly, yet most people still assume solar requires a large upfront payment. This guide from Discount Solar breaks down every financing path available in 2026, including how NEM 3.0 changes the math and why battery storage now matters more than ever. Below, we’ll show you exactly how to choose the right option, claim the incentives you qualify for, and avoid the mistakes that cost homeowners thousands.

The bottom line most guides bury: zero-down solar is real, but not all zero-down paths are equal. A solar loan and a solar lease both require no money up front, but one builds equity and keeps your tax credits, while the other does neither.

Why Zero Down Solar Options in Kern County Make Sense Right Now

Kern County averages more than 270 sunny days per year, making it one of the strongest solar markets in the state. That raw solar resource translates directly into system output, which is the core variable that determines how fast any solar investment pays back.

The financial case has also shifted. Electricity rates from Pacific Gas and Electric and Southern California Edison have risen steadily over the past several years, and Kern County residents on tiered rate structures feel that pressure most during summer months when air conditioning loads spike. Locking in a fixed solar payment today is a hedge against rates that are likely to keep climbing.

What most people get wrong here is the assumption that zero down means zero benefit. A properly structured solar loan lets you own the system outright while paying nothing at closing. The federal Investment Tax Credit then reduces your tax liability in the year you install, effectively lowering the total system cost by a meaningful margin. That combination, no upfront cash plus a significant tax credit, is why zero down solar financing has become the dominant path for Kern County homeowners in 2026.

Kern County Utility Rates and What They Mean for Your Savings

Utility rates in Kern County vary depending on your provider, but many residential customers fall under PG&E or SCE territory, both of which have implemented rate increases in recent years. The higher your current electricity bill, the faster a solar system pays back, regardless of financing method.

The practical implication: homeowners with monthly bills above a certain threshold tend to see the strongest financial case for solar. A solar system sized to offset most of your consumption converts what was a recurring utility expense into a fixed monthly loan payment, often at a lower monthly cost than the electricity bill it replaces. According to U.S. Energy Information Administration electricity rate data, California consistently ranks among the highest-cost states for residential electricity, which strengthens the solar value proposition for Kern County residents specifically.

Pro TipBefore you request a solar quote, pull your last 12 months of electricity bills. Installers use your annual kilowatt-hour consumption to size your system correctly. Oversizing wastes money; under sizing leaves you still paying the utility.

Solar Lease vs Purchase Pros and Cons for Kern County Homeowners

The single most consequential decision in your solar process is not which panels to buy. It is whether you own the system or rent it. Every other variable flows from that choice, and under NEM 3.0, that choice carries more financial weight than it did even three years ago.

| Option | Upfront Cost | You Own the System | Federal Tax Credit | NEM 3.0 Battery Benefit | Long-Term Savings |

|---|---|---|---|---|---|

| Solar Loan | $0 | Yes | Yes (full credit to you) | Yes, you capture battery arbitrage value | Highest |

| Solar Lease | $0 | No | No (goes to lessor) | Partial, lessor may not optimize for your TOU rate | Moderate |

| PPA | $0 | No | No | Partial, depends on contract structure | Moderate |

| Cash Purchase | Full cost | Yes | Yes | Yes | Highest (no interest cost) |

Zero Down Solar Loan: Own Your System, Keep the Incentives

A zero down solar loan is the best financing option for most Kern County homeowners who qualify. The loan covers the full system cost, you take ownership immediately, and the federal Investment Tax Credit flows directly to you. Many borrowers apply their tax credit to the loan principal in year one, which reduces the outstanding balance and can meaningfully lower ongoing monthly payments.

Loan terms typically range from 10 to 25 years, with APR varying based on credit score and lender. Here is the trade-off most installers gloss over: a 10-year loan at a higher monthly payment will cost substantially less in total interest than a 25-year loan at a lower monthly payment. On a system in the mid-five-figure range, the difference in total interest paid between a 10-year and a 25-year term can exceed the value of the federal tax credit itself. Run both scenarios before signing.

Ownership also matters under NEM 3.0 specifically. Because the new export rate structure rewards self-consumption over grid export, the homeowner who owns their system, and can add battery storage at any point, has full control over optimizing their energy dispatch strategy. A loan borrower can add a battery mid-term and claim the federal ITC on that storage addition. A lease customer cannot make that decision unilaterally; any system modification requires lessor approval.

At resale, owned solar systems add appraised value to a home. A leased system transfers the lease obligation to the buyer, which requires buyer qualification with the leasing company and can complicate or derail a sale, a documented friction point in California real estate transactions.

Solar Lease and PPA: Low Risk, Lower Reward, and a NEM 3.0 Complication

A solar lease and a Power Purchase Agreement (PPA) are structurally similar: a third-party company owns the panels on your roof, and you either pay a fixed monthly lease fee or a per-kilowatt-hour rate for the electricity produced. Both require zero down.

The honest limitations are significant, and NEM 3.0 has added a new one. You do not receive the federal tax credit. You do not build equity. You are locked into a contract, often 20 to 25 years, with annual escalator clauses that can increase your payments by a fixed percentage each year regardless of what utility rates actually do. Exiting early typically involves a buyout calculated on the remaining contract value, which can be substantial in the first decade.

The NEM 3.0 complication: under the old export structure, a lease or PPA could still deliver meaningful savings because the lessor’s system was generating credits close to retail value. Under NEM 3.0, export credits are substantially lower, which compresses the savings margin for grid-tied-only systems. If your lease or PPA does not include battery storage, and most entry-level lease products do not, you are now in a structure that was designed for a policy environment that no longer exists for new customers.

Leases and PPAs make sense in a narrow set of circumstances: homeowners who cannot use the federal tax credit due to low tax liability, those with roof or structural situations that make ownership complicated, or those who want zero maintenance involvement and have reviewed the escalator terms carefully. For the majority of Kern County homeowners with standard tax liability and a qualifying roof, a solar loan is the better path.

Watch OutBefore signing any lease or PPA, calculate the total payments over the full contract term including all escalator increases. Compare that total to the total cost of a solar loan for the same system. The monthly payment on a lease may look lower, but the 25-year total cost comparison often tells a different story.

The NEM 3.0 Ownership Advantage in Plain Terms

Here is the practical summary of why ownership matters more under NEM 3.0 than it did under NEM 2.0. Under the old structure, exporting excess solar to the grid at near-retail rates meant even a lease customer captured most of the system’s value. Under NEM 3.0, the value of solar has shifted from export credits to self-consumption and battery storage arbitrage. The homeowner who owns their system controls how that value is captured. The lease customer does not. That structural shift is the single most underreported reason why the loan-vs-lease calculus has changed since April 2023.

Solar Tax Credits California: What You Can Claim in 2026

California solar customers in 2026 have access to multiple incentive layers that can be stacked to reduce your net system cost significantly, even when financing with zero down. The key is understanding not just what each incentive is, but the order in which to apply them and how NEM 3.0 changes which incentives deliver the most value.

Federal Investment Tax Credit (ITC): Mechanics That Actually Matter

The federal Investment Tax Credit is a credit against your federal income tax liability equal to a percentage of your total solar system cost, including installation. For residential systems installed in 2026, the ITC remains in effect under current federal energy legislation. The credit applies to owned systems only, which is why solar loan financing preserves this benefit while leases do not.

A common mistake is confusing a tax credit with a tax deduction. A credit reduces your tax bill dollar for dollar. A deduction only reduces your taxable income. If your ITC credit exceeds your tax liability in year one, the remaining credit can typically be carried forward to subsequent tax years under current IRS rules.

According to IRS guidance on residential clean energy credits, the credit applies to the cost of solar panels, labor, inverters, mounting hardware, and battery storage when installed as part of the solar system. That last point, battery storage, is critical under NEM 3.0.

The ITC and battery storage under NEM 3.0: Because NEM 3.0 makes self-consumption more valuable than grid export, adding battery storage to your system is now a financially strategic decision, not just a backup-power convenience. When a battery is installed as part of your solar project, its full cost is included in the ITC calculation. This means the federal government is effectively subsidizing a portion of the battery system that will then help you arbitrage your utility’s time-of-use rates for the life of the system. Homeowners who install solar-only now and add a battery later may still qualify for the ITC on the battery addition, but the paperwork and qualification requirements are more complex. Installing both together in a single project is the cleaner path.

Keep all installation contracts, itemized invoices, and equipment receipts. You will file IRS Form 5695 with your federal return in the year of installation. If your installer provides a single lump-sum contract, request an itemized breakdown, it documents the eligible cost basis for the credit.

California SGIP Battery Rebate: The Incentive Most Homeowners Miss

California does not currently offer a statewide solar panel rebate, but the Self-Generation Incentive Program (SGIP) continues to offer rebates specifically for battery storage systems, and under NEM 3.0, this is arguably the most strategically important incentive available to Kern County homeowners.

SGIP is administered by the California Public Utilities Commission and funded through utility ratepayers. It is structured in tiers, and the rebate amount per watt-hour of storage capacity varies by which tier you qualify for:

- General Market tier: Available to most residential customers. Rebate levels fluctuate as funding tranches are released and exhausted. Check current availability with your installer before assuming this tier is open.

- Equity tier: Available to customers in low-income households or those enrolled in utility low-income assistance programs such as CARE or FERA. Kern County has a meaningful population of CARE-eligible households, and the equity tier rebate is substantially higher than the general market rate. If you are on a CARE or FERA rate, ask your installer specifically about equity tier eligibility before accepting a general market quote.

- Equity Resiliency tier: The highest rebate level, reserved for customers in high fire-threat districts or those who have experienced two or more public safety power shutoff events. Portions of Kern County’s foothill and rural areas qualify. Verify your address against the CPUC’s high fire-threat district map.

SGIP funding is released in tranches and can be exhausted mid-year. Waiting to apply can mean losing access to a rebate that was available when you got your quote. A reputable installer will submit your SGIP reservation as part of the project initiation process, not as an afterthought.

California Property Tax Exclusion: The Long-Tail Benefit

California law excludes the added value of a solar installation from property tax assessments. This means your property taxes do not increase when you add solar, despite the system adding appraised value to your home. As documented in California State Board of Equalization solar property tax exclusion, this exclusion applies to active solar energy systems and is a meaningful long-term financial benefit that compounds over the life of the system.

This exclusion is not automatic in all cases, confirm with your Kern County assessor that the exclusion has been applied after your system is permitted and installed.

How to Stack These Incentives Correctly

The order of operations matters because each incentive affects your net cost basis differently:

Step 1, Size your system to include battery storage if NEM 3.0 applies to you. Including storage in the original project maximizes your ITC-eligible cost basis and simplifies SGIP application.

Step 2, Apply for SGIP reservation early. Your installer should submit this at project initiation. The SGIP rebate reduces your out-of-pocket or financed system cost before the ITC is calculated, meaning a lower loan balance if you apply the rebate at closing.

Step 3, Claim the federal ITC on your tax return for the year of installation. File Form 5695. If you financed with a solar loan and plan to apply your tax credit to the loan principal, coordinate the timing with your lender, most solar loan products have a specific window (often 12 to 18 months post-installation) during which a principal payment from the tax credit can reduce your ongoing monthly payment.

Step 4, Confirm your property tax exclusion with the Kern County Assessor’s Office. This is a passive long-term benefit, but verifying it is applied correctly takes one phone call and protects you from an unexpected assessment increase.

Key TakeawayThe most common incentive mistake Kern County homeowners make is treating the ITC and SGIP as separate decisions. They are not. A solar-plus-storage system installed as a single project captures the ITC on both components and qualifies for SGIP in one application. Splitting the projects into two phases typically reduces your total incentive capture and adds administrative complexity.

A Note on Incentive Documentation After Installer Closures

The SunPower bankruptcy highlighted a documentation risk that applies to incentives as well as warranties. If your installer closes before your SGIP rebate is processed or before your interconnection is complete, your incentive applications can be delayed or lost. When you work with any installer, confirm that your SGIP reservation number and interconnection application reference number are provided to you in writing before installation begins. These are your records, not just the installer’s, and having them means you can follow up with the utility and CPUC directly if your installer becomes unavailable.

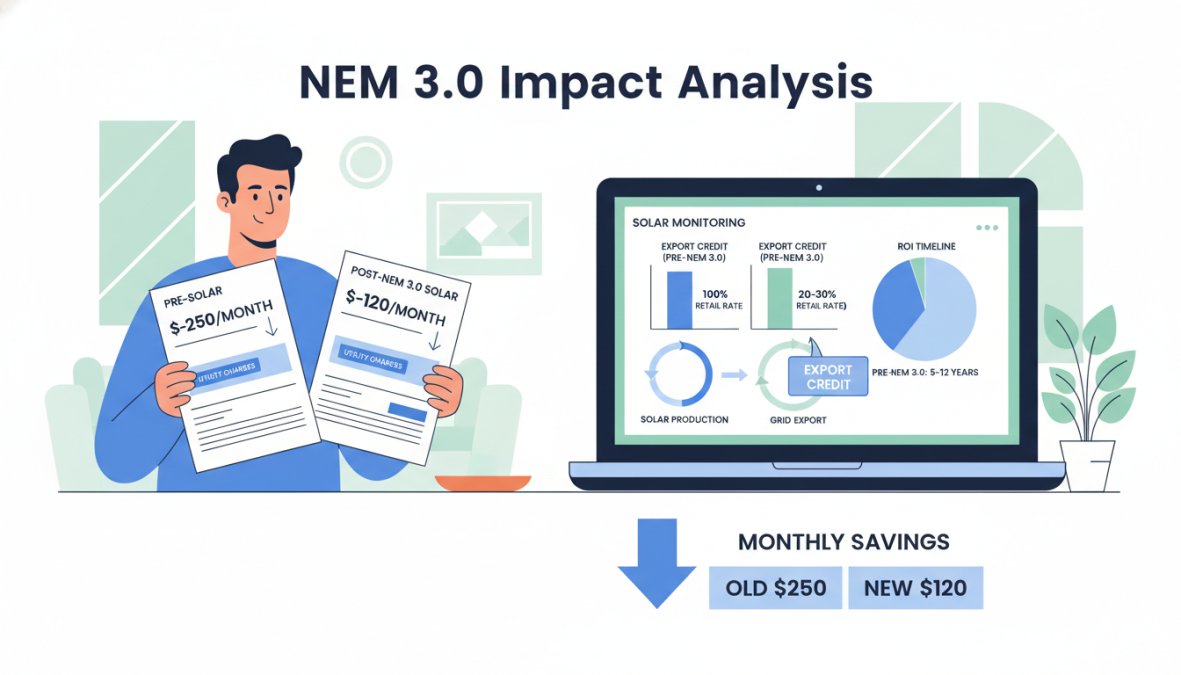

NEM 3.0 Impact Analysis: How It Changes Zero Down Solar ROI

NEM 3.0 is the most significant policy shift to hit California solar in a decade, and most zero down solar guides still haven’t caught up to what it actually means for Kern County homeowners deciding in 2026.

Net energy metering is the policy that determines how much your utility pays you for excess solar electricity you send back to the grid. Under NEM 2.0, that credit was close to the retail rate, making grid-tied systems highly profitable. Under NEM 3.0, which took effect for new applicants in April 2023, the export credit rate dropped substantially, averaging around 75% less than under the previous structure.

The practical result: a solar-only system under NEM 3.0 takes longer to pay back than it did under NEM 2.0. The system still saves money, but the economics favor consuming your own solar production rather than exporting it.

Solar Battery Storage ROI Under NEM 3.0

This is where the analysis gets interesting. Battery storage, which was previously a nice-to-have, has become a financially strategic addition under NEM 3.0. Here’s the logic: instead of exporting excess solar at a low NEM 3.0 credit rate, you store that energy in a battery and use it during evening peak hours when utility rates are highest.

The ROI on battery storage under NEM 3.0 depends on your utility’s time-of-use rate structure. Customers on time-of-use plans with high peak-hour rates see the strongest battery ROI, because the battery effectively arbitrages the difference between the low export credit and the high peak retail rate.

California’s SGIP rebate can offset a meaningful portion of battery system costs. Homeowners in Kern County should check current SGIP equity and equity resiliency budget availability, as funding is released in tranches and can be exhausted. The combination of SGIP rebate plus the federal ITC applying to battery storage makes the all-in cost of a solar-plus-storage system more competitive than it appears at the sticker price.

Watch OutDo not size your battery based on what looks good on paper. Your installer should model your specific time-of-use rate, consumption pattern, and solar production profile. A battery sized for the wrong use case will underperform and extend your payback period.

How to Qualify for Solar Financing in Kern County

Solar financing qualification follows similar logic to other secured lending, but with some solar-specific nuances worth understanding before you apply.

Lenders evaluate credit score, debt-to-income ratio, and home equity. Credit score thresholds vary by lender and product, but many solar loan programs are accessible to borrowers with scores in the mid-600s and above. Borrowers with stronger credit profiles access lower APR options, which materially affects total cost over a 20-year loan term.

Home ownership is required. Renters cannot apply for solar financing on a property they do not own. For homeowners with equity, some lenders offer secured solar loans that carry lower rates than unsecured options.

Step-by-Step: Getting Started with Zero Down Solar

Getting started is more straightforward than most people expect. The process from first contact to installation typically takes four to eight weeks, depending on permit timelines in your jurisdiction.

Step 1: Gather your electricity bills. Collect 12 months of bills to establish your annual consumption baseline. Your installer needs this to size your system accurately.

Step 2: Request a solar quote. A reputable installer will perform a site assessment, review your roof condition and orientation, and provide a detailed proposal with system size, projected production, and financing options.

Step 3: Review financing options. Compare loan terms, APR, and total cost of ownership across options. Confirm whether the loan is secured or unsecured and check for prepayment penalties.

Step 4: Submit your financing application. Most solar lenders run a soft credit pull for pre-qualification and a hard pull only upon final approval.

Step 5: Sign contracts and permit. Your installer handles permits with the local building department and utility interconnection applications.

Step 6: Installation and inspection. Certified installers complete the physical installation. A city inspector signs off, and your utility activates the system for grid interconnection.

Step 7: Claim your tax credit. File IRS Form 5695 with your federal tax return in the year of installation to claim the Investment Tax Credit.

According to California Energy Commission solar installation guidance, working with certified installers who are licensed by the California Contractors State License Board is a baseline requirement for permit approval and warranty protection.

Post-SunPower Bankruptcy: Choosing a Reliable Installer for Zero Down Solar Options in Kern County

SunPower’s 2024 bankruptcy filing sent a clear message to the California solar market: installer longevity is not guaranteed, and choosing a company based on brand recognition alone carries real risk. Homeowners who installed with SunPower found themselves navigating warranty claims with a company in financial distress, a situation that underscores why vetting your installer matters as much as vetting your financing.

The right question to ask any installer is not just “how long have you been in business” but “who backs your equipment warranty if your company closes.” A 25-year warranty is only as strong as the entity standing behind it.

Discount Solar has operated in Bakersfield and Kern County for over a decade, with a 25-year equipment warranty backed directly by the company and its manufacturer partners. The team consists of certified installers who handle custom solutions across both straightforward and complex residential configurations. That track record and warranty structure matter more in a post-SunPower market than they did five years ago.

When evaluating any installer for zero down solar options Kern County homeowners should check:

- California CSLB license status (verify at the state licensing board)

- Years of local operation and references from Kern County installations

- Who manufactures the panels and inverters, and what the manufacturer warranty covers independently

- Whether the installer’s warranty survives a company acquisition or closure

Benefits of Switching to Residential Solar in Bakersfield and Kern County

The financial case for residential solar in Kern County is strong, but the benefits extend beyond the monthly bill comparison.

Energy independence. A solar-plus-storage system reduces your dependence on the grid during peak demand periods and outages. Kern County’s summer heat waves create exactly the grid stress conditions where battery backup provides real value, keeping critical loads running when the utility is under strain.

Reduced carbon footprint. Kern County’s grid still draws substantially from fossil fuels. Residential solar directly displaces that generation, reducing your household’s carbon footprint without requiring any lifestyle changes. For homeowners who care about sustainable energy and clean energy goals, solar is among the highest-impact individual actions available.

Long-term cost predictability. Utility rates are set by regulators and can increase without your input. A fixed solar loan payment does not change. Over a 20-25 year system lifespan, that predictability has compounding financial value as utility rates continue their historical upward trend.

Home value. Owned solar systems are recognized by appraisers and have been shown in multiple housing market analyses to add resale value. The California property tax exclusion means you capture that value without a corresponding increase in your annual tax bill.

Durability. Modern solar panels from reputable manufacturers carry 25-year performance warranties, meaning the system is designed to produce meaningful output for the full financing term and beyond. Discount Solar’s 25-year equipment warranty reflects this industry standard and gives homeowners a clear accountability structure if panels underperform.

The combination of immediate bill reduction, long-term rate protection, energy independence, and environmental benefit makes residential solar in Bakersfield and Kern County one of the most defensible home investments available in 2026.

Choosing the right zero down solar path in Kern County requires navigating financing structures, NEM 3.0 policy changes, battery storage economics, and installer reliability simultaneously. Discount Solar brings over a decade of local experience, certified installation teams, and a 25-year equipment warranty to every project in Bakersfield and Kern County. Get your estimate from Discount Solar and start replacing your utility bill with a fixed solar payment that works in your favor.

Frequently Asked Questions

How does zero down solar work in California?

Zero down solar in California means you can go solar with no upfront payment through financing options like solar loans, leases, or power purchase agreements (PPAs). With a solar loan, you own the system and keep tax credits and incentives. With a lease or PPA, a third party owns the panels and you pay a fixed monthly amount. Either way, your monthly solar payment is typically lower than your previous electricity bill, creating immediate savings on clean energy.

Are there solar incentives available in Kern County?

Yes. Kern County homeowners can access the federal Investment Tax Credit (ITC), which currently allows you to deduct a significant percentage of your solar installation cost from federal taxes. California also offers property tax exclusions for solar additions and, in some cases, local utility rebates. When combined with zero down solar financing, these solar tax credits in California can substantially reduce the total cost of going solar and improve your long-term return on investment.

What are the pros and cons of solar leases vs. solar loans?

A solar loan lets you own your system, qualify for the federal tax credit, and build equity, but you take on debt with monthly payments and an APR. A solar lease requires no ownership responsibility and often includes maintenance, but you forfeit tax credits and save less over time since the installer owns the panels. For most Kern County homeowners who qualify for financing, a loan typically delivers better long-term savings than a lease or PPA arrangement.

Do I qualify for zero down solar programs in Kern County?

Qualification for zero down solar financing generally depends on your credit score, home ownership status, and income. Most solar loan programs look for a credit score of 620 or above, though some lenders have lower thresholds. Leases and PPAs often have more flexible credit requirements. A certified installer like Discount Solar can review your situation, walk you through available options, and help you get a solar quote that fits your budget with no upfront cost required.

Is solar worth it in Bakersfield and Kern County after NEM 3.0?

Yes, but the math has shifted. Under NEM 3.0, export rates for excess solar energy sent to the grid are lower than under previous rules, which reduces bill credits. However, Kern County’s high sun exposure and rising utility rates still make solar a strong investment. Pairing solar panels with battery storage helps you maximize self-consumption rather than exporting power, improving ROI under NEM 3.0. A 25-year warranty on equipment ensures long-term durability and reliable savings.